The difference between the sale price and the cost of merchandise is the profit of the business that would increase the owner’s equity by $1,000 (6,000 – $5,000). For every business, the sum of the rights to the properties is equal to the sum of properties owned. Drawings are amounts taken xero accounting integration out of the business by the business owner. In other words, all assets initially come from liabilities and owners’ contributions. Before taking this lesson, be sure to be familiar with the accounting elements. To learn more about the income statement, see Income Statement Outline.

Get Your Questions Answered and Book a Free Call if Necessary

Because there are two or more accounts affected by every transaction, the accounting system is referred to as the double-entry accounting or bookkeeping system. You can find a company’s assets, liabilities, and equity on key financial statements, such as balance sheets and income statements (also called profit and loss statements). These financial documents give overviews of the company’s financial position at a given point in time. The accounting equation ensures the balance sheet is balanced, which means the company is recording transactions accurately. Income and expenses relate to the entity’s financial performance. Individual transactions which result in income and expenses being recorded will ultimately result in a profit or loss for the period.

What Are the 3 Elements of the Accounting Equation?

At the same time, it incurred in an obligation to pay the bank. An error in transaction analysis could result in incorrect financial statements. Whether you call it the accounting equation, the accounting formula, the balance sheet equation, the fundamental accounting equation, or the basic accounting equation, they all mean the same thing.

Owners Equity (or Equity)

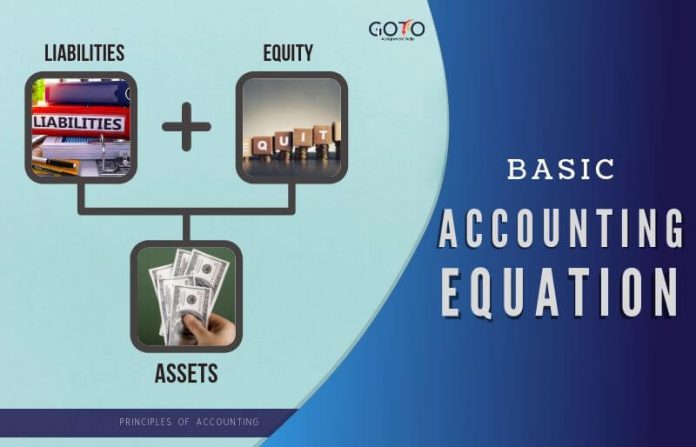

Additionally, analysts can see how revenue and expenses change over time, and the effect of those changes on a business’s assets and liabilities. The accounting equation states that total assets is equal to total liabilities plus capital. This lesson presented the basic accounting equation and how it stays equal. The fundamental accounting equation, also called the balance sheet equation, is the foundation for the double-entry bookkeeping system and the cornerstone of accounting science. In the accounting equation, every transaction will have a debit and credit entry, and the total debits (left side) will equal the total credits (right side). In other words, the accounting equation will always be “in balance”.

- Assets pertain to the things that the business owns that have monetary value.

- Think of retained earnings as savings, since it represents the total profits that have been saved and put aside (or “retained”) for future use.

- To make the Accounting Equation topic even easier to understand, we created a collection of premium materials called AccountingCoach PRO.

- To calculate the accounting equation, we first need to work out the amounts of each asset, liability, and equity in Laura’s business.

- 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements.

Question 1

Because all accounting entries – all of them – are derived from it. Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals. A financial professional will be in touch to help you shortly.

If the left side of the accounting equation (total assets) increases or decreases, the right side (liabilities and equity) also changes in the same direction to balance the equation. Because it considers assets, liabilities, and equity (also known as shareholders’ equity or owner’s equity), this basic accounting equation is the basis of a business’s balance sheet. The income statement is the financial statement that reports a company’s revenues and expenses and the resulting net income.

Owner’s or stockholders’ equity also reports the amounts invested into the company by the owners plus the cumulative net income of the company that has not been withdrawn or distributed to the owners. Incorrect classification of an expense does not affect the accounting equation. An asset is a resource that is owned or controlled by the company to be used for future benefits. Some assets are tangible like cash while others are theoretical or intangible like goodwill or copyrights.

The owner’s equity is the balancing amount in the accounting equation. So whatever the worth of assets and liabilities of a business are, the owners’ equity will always be the remaining amount (total assets MINUS total liabilities) that keeps the accounting equation in balance. The accounting equation is based on the premise that the sum of a company’s assets is equal to its total liabilities and shareholders’ equity. As a core concept in modern accounting, this provides the basis for keeping a company’s books balanced across a given accounting cycle. As you can see, no matter what the transaction is, the accounting equation will always balance because each transaction has a dual aspect.

On the other hand, double-entry accounting records transactions in a way that demonstrates how profitable a company is becoming. Investors are interested in a business’s cash flow compared to its liability, which reflects current debts and bills. The accounting equation is not always accurate if it is unbalanced. This can lead to inaccurate reporting of financial statements and incorrect decisions made by management regarding money and investment opportunities.

In above example, we have observed the impact of twelve different transactions on accounting equation. Notice that each transaction changes the dollar value of at least one of the basic elements of equation (i.e., assets, liabilities and owner’s equity) but the equation as a whole does not lose its balance. The accounting equation equates a company’s assets to its liabilities and equity. This shows all company assets are acquired by either debt or equity financing.